The shift toward turnover-linked and hybrid leasing structures is now firmly embedded across retail real estate. For most institutional landlords, the discussion is no longer about whether to adopt performance-linked income models, but how to manage them effectively at scale.

Across the UK and Europe, turnover-based rent mechanisms have become standard in many retail and leisure portfolios, reflecting a more collaborative alignment between landlord and occupier. At the same time, physical retail assets have attracted renewed investment attention, supported by improved trading resilience and selective capital reallocation back into well-performing locations. These developments reinforce the commercial logic of performance-linked leases, but they also increase the operational demands placed on landlords.

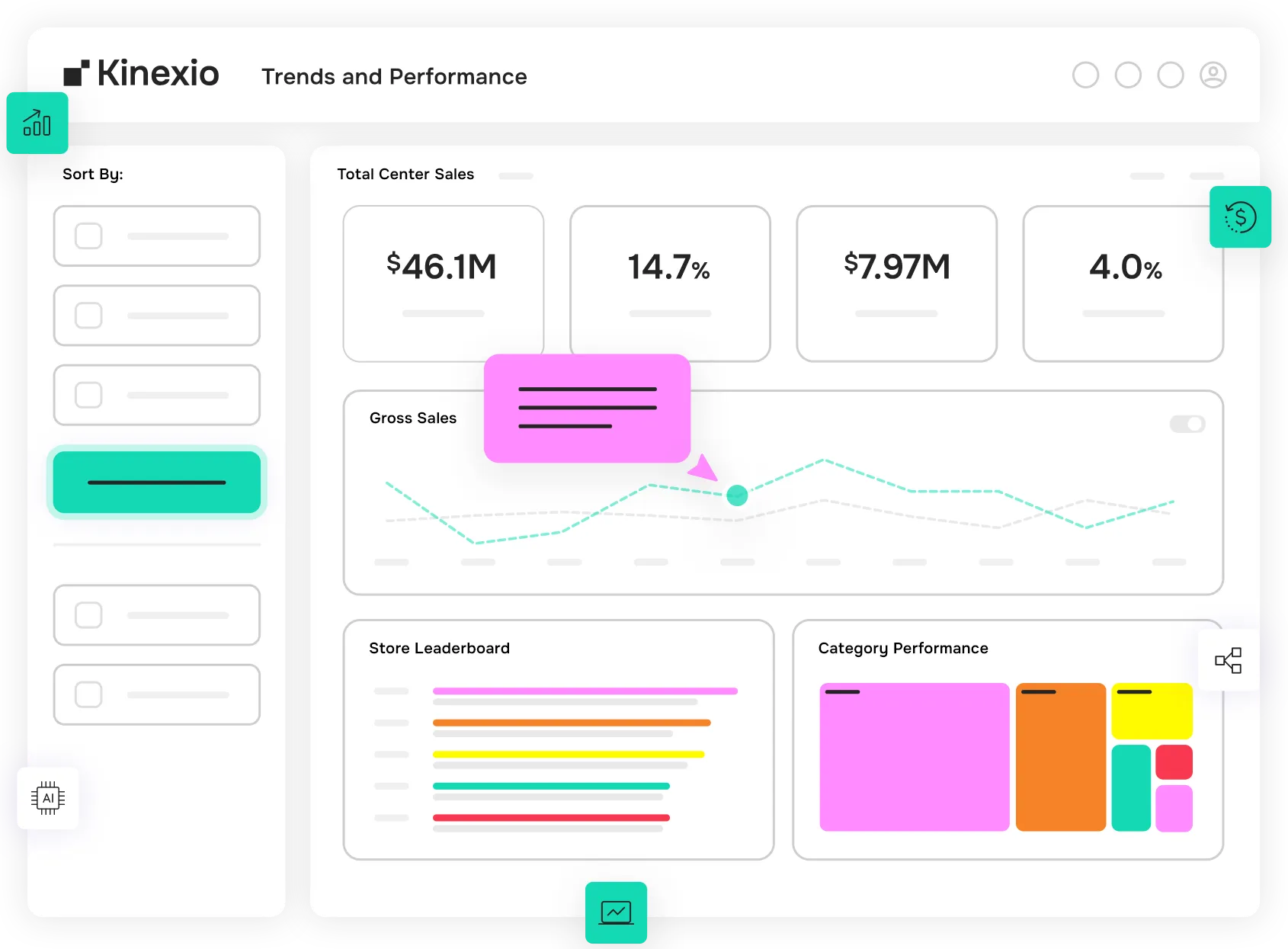

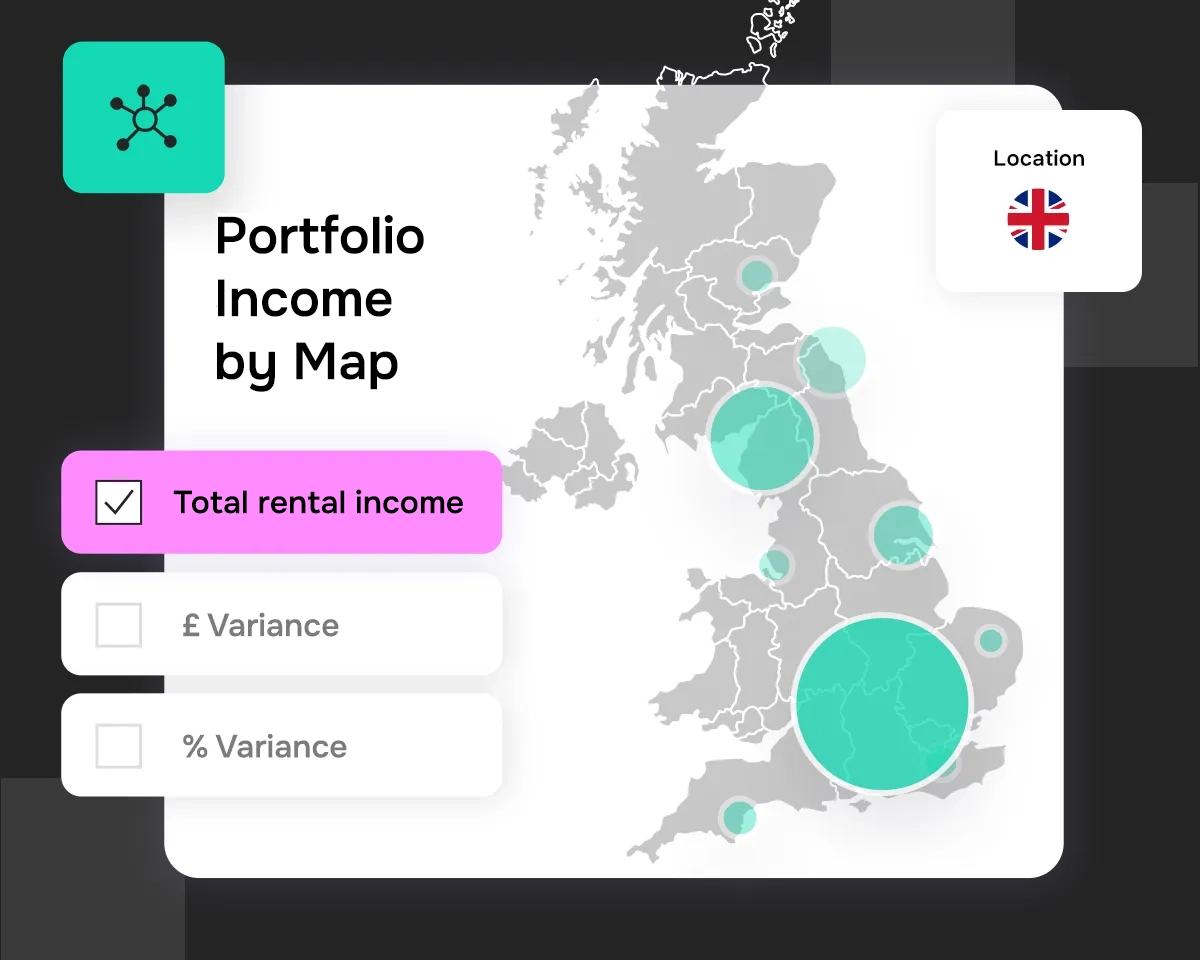

When rental income is directly influenced by tenant turnover, the quality and immediacy of performance data becomes central to portfolio management. Income forecasting, valuation assumptions, and asset strategy increasingly depend on reliable sales reporting and consistent compliance with lease terms.

Under traditional fixed-rent models, reporting cycles were less time-sensitive. Variations in tenant performance did not immediately affect landlord income. Turnover-linked structures introduce greater sensitivity. A delay in receiving accurate sales data can affect accruals, forecasts, and internal reporting. Inconsistent data formats across assets make portfolio comparison more complex and reduce confidence in aggregated performance metrics.