As the dust settles on a turbulent few years in commercial real estate, 2026 is shaping up to be a defining moment a year of cautious recovery, structural divergence, and deeply strategic capital. But how that plays out will look very different in Europe versus North America.

1. Macro backdrop & real estate capital flows: Optimism, but with regional nuance

According to recent Deloitte research, about 70% of European CRE executives expect improvements in leasing, capital markets, and lending through 2026 a significantly more optimistic outlook than their North American counterparts.

In Europe, this optimism is underpinned by improving stability. The commercial real estate market is slowly stabilising, despite macro-political risks, with Cushman & Wakefield reporting a 7.4% year-on-year rebound in transaction volumes in H1 2025 led by Germany and the UK. Meanwhile, according to MSCI data, North American markets are still digesting high borrowing costs and refinancing risk: Deloitte highlights that many loans underwritten during the era of cheap debt (e.g., around 3.9%) are now maturing or resetting into significantly higher rate environments.

This divergence means capital reallocation will be highly selective in 2026: European players are increasingly bullish on core markets, while North American investors will lean into risk-adjusted deals, especially in sectors with resilience.

2. Retail real estate: the “winners” are separating from the middle

If 2025 proved anything, it’s that retail isn’t simply “back”, it’s polarising. The strongest assets are behaving like scarce infrastructure: they’re absorbing demand, pushing rents, and pulling investment back into the sector. The rest are still wrestling with thin occupier demand, higher operating costs, and a consumer that is choosier than ever.

-

Winner #1: Retail destinations with genuine scarcity (and a flight-to-quality tailwind)

Across markets, the story isn’t blanket recovery, it’s competition for the best space. In the U.S., national retail vacancy sat at 5.8% in Q3 2025, with rents still rising year-on-year even as demand cooled from earlier peaks; a sign that, in prime locations, landlords still hold pricing power.

JLL also points to a turn in momentum in Q3 2025, with positive net absorption of 4.7 million sq ft, as the market stabilises after store closures, against a backdrop of severely constrained new supply.

Translation: the best retail corridors and centres are benefiting from the same “quality is king” dynamic you’ve already outlined for offices, just with stronger consumer demand underneath it.

-

Winner #2: Formats built for convenience and repeat visits (where footfall is still defendable)

Footfall in 2025 has been volatile, but the granularity matters. UK BRC-Sensormatic data shows that when you adjust for calendar distortion, retail parks were the strongest performer: across March and April 2025 combined, retail park footfall rose 2.7% YoY, versus -0.7% for shopping centres.

That gap speaks to what’s working on the ground: value, convenience, car access, and “mission” shopping, supported by retailers that can trade through a cautious consumer environment.

-

Winner #3: Retail that behaves like a living operating system (data-led landlords)

A quieter “winner” in 2025 has been the operationally sophisticated landlord: owners using leasing intelligence, trading performance signals, and customer insight to keep assets relevant (and to defend NOI when consumer demand softens). The occupier mix trends hint at this shift.

Cushman & Wakefield’s European analysis of H1 2025 lettings shows:

- Fashion remained dominant, accounting for 37% of leased floorspace (H1 2025).

- Mixed Goods expanded sharply, with leased space up 55% and letting transactions up 33% YoY (H1 2025 vs H1 2024).

- Luxury lettings increased by over 50% YoY in H1 2025, with activity particularly in Italy and the UK.

This is the “winners” lens in practice: assets that can curate demand — and prove it — are the ones attracting the most resilient brands, the most flexible deal structures, and the strongest repeat visitation.

3. Commercial offices: quality is king (but bedrooms differ)

In both Europe and North America, the office market is bifurcating sharply, but for somewhat different reasons.

In Europe, CBRE notes that office attendance is rising, with over 60% of companies reporting average in-office attendance between 41–80%, up significantly from prior years. Tenant demand is skewing heavily toward prime, modern buildings, leading to a widening vacancy gap between high-quality and secondary stock. At the same time, Savills forecasts European office development will drop to just 3.1 million m² in 2026, the lowest since 2017, with speculative completions now down to only 1.6%. That constrained supply of new speculative product could buoy prime rents and drive up the value of well-located, ESG-aligned offices.

In North America, the story is more mixed. While some markets are showing net absorption, many legacy properties (especially older, suburban Class B and C) continue to face demand risk. The winners will likely be high-quality, sustainable offices. Investors may double down on repositioning or retrofitting older assets to meet occupier expectations, particularly in dense urban cores.

4. Data centres, AI & alternative assets: the structural winners

One of the most compelling cross-regional stories for 2026 is the surge in digital infrastructure, especially data centres.

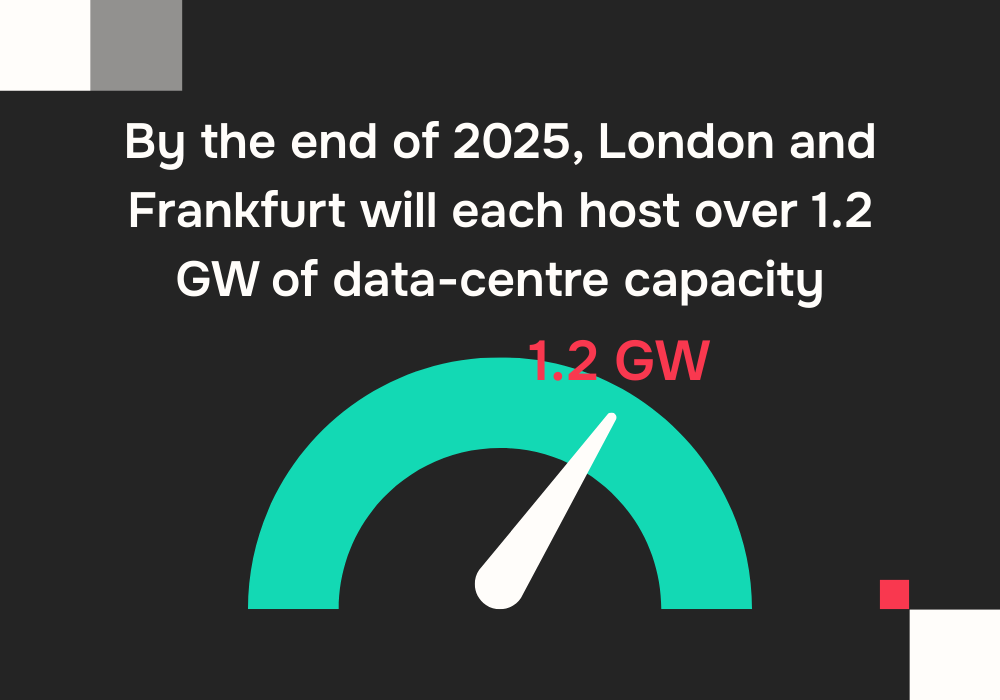

- Europe: CBRE projects that by the end of 2025, London and Frankfurt will each host over 1.2 GW of data-centre capacity, accounting for nearly half of Europe’s total pipeline. At the same time, vacancy across the major 15 European data centre markets is expected to hit just 9%, down significantly as hyperscaler demand and constrained development continue.

- North America: The U.S. and Canadian markets are already deeply established but continue to benefit from AI-driven demand, cloud expansion, and long-duration leases. Investors will likely keep chasing capacity-light hyperscale space, especially where power and land constraints limit new builds.

Beyond data centres, both markets are also seeing interest in life sciences real estate, residential alternatives (build-to-rent, multifamily), and ESG-anchored adaptive uses, signalling capital flows toward structurally growing subsectors.

5. Real estate debt, refinancing risk & ESG retrofit play

Refinancing risk is arguably the single biggest near-term threat heading into 2026, but both Europe and North America have levers to manage it.

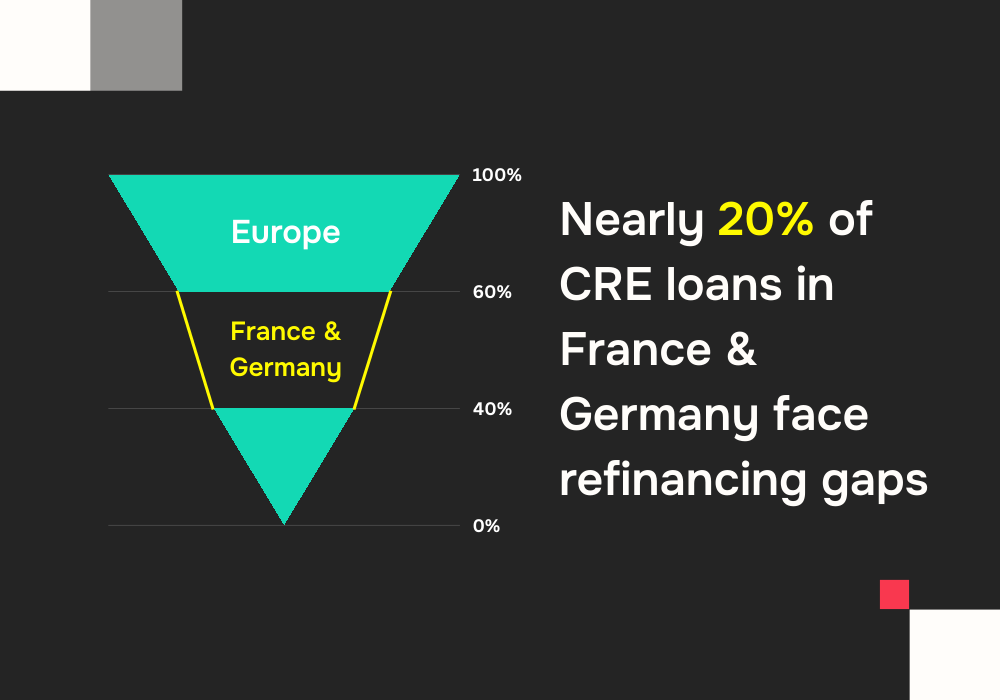

- Refinancing exposure: Deloitte’s analysis highlights that many loans taken out in 2022 (when rates were very low) are now maturing into much more expensive debt. In Europe, certain markets like Germany and France are particularly exposed: nearly 20% of CRE loans in those markets face refinancing gaps, according to Deloitte’s survey.

- Alternative debt sources: As a response, CRE leaders in both regions are increasingly tapping private credit, private equity, and insurance-backed lending.

- Retrofit & ESG value: The cost of capital may be steep, but assets with strong ESG credentials offer a compelling edge. Whether it’s reducing energy consumption in European offices or upgrading aging U.S. industrial assets, investors who prioritize retrofit risk will have more optionality, either to hold with better cash flow or to reposition for conversion.

6. Regional risk factors, and what could derail the recovery

Europe: The markets remain exposed to macro-political risk, especially with rising trade tensions and regulatory complexity. More than that, while prime office rents are rising (Knight Frank reports 8.9% y/y growth in European prime office rents in Q2 2025), volume remains restrained. In H1 2025, MSCI reported €91.7 bn in CRE investment across Europe, down 7% year-on-year.

North America: High interest rates, refinancing cliffs, and debt service stress remain significant challenges. As Deloitte notes, many borrowers are poorly positioned to repay or refinance under the current market conditions.

Balanced optimism with structural sharpness

2026 is not likely to usher in a full-blown boom for commercial real estate, but it does promise selective, meaningful recovery. The winners will be those who understand that this is not a simple bounce-back: it’s a structural re-rating. In both Europe and North America, quality, sustainability, and flexibility will drive value.